9MFY24 PAT at `17,732 crores up 16% YOY, consolidated ROE at 18.86% up 82 bps YOY

IBPC: Inter Bank Participation Certificates

QAB: Quarterly Average Balance

MAU: Monthly Active Users engaging in financial and non-financial transactions

1 SBB : Small Business Banking

2 Based on RBI data as of Nov'23

3 across 64 global banks, 82 fintechs and 9 neo banks with 2.4 mn+ reviews

4 Coverage Ratio = Aggregate provisions (specific + standard + additional + Covid) / IRAC GNPA

* including profits for 9MFY24, net organic accretion = capital accreted – capital consumed (excluding consumption for regulatory changes in risk weights)

Snapshot (As on December 31st, 2023) (in ` Crores)

| Profit & Loss | Absolute (in ` Crores) | QOQ | YOY Growth | |||

|---|---|---|---|---|---|---|

| Q3FY24 | Q2FY24 | 9MFY24 | Q3FY24 | Q3FY24 | 9MFY24 | |

| Net Interest Income | 12,532 | 12,315 | 36,805 | 2% | 9% | 18% |

| Fee Income | 5,169 | 4,963 | 14,620 | 4% | 29% | 29% |

| Operating Expenses | 8,946 | 8,717 | 25,894 | 3% | 32% | 32% |

| Operating Profit | 9,141 | 8,632 | 26,587 | 6% | (1%) | 16% |

| Core Operating Profit | 8,850 | 8,733 | 25,878 | 1% | - | 12% |

| Profit after Tax | 6,071 | 5,864 | 17,732 | 4% | 4% | 16% |

| Balance Sheet | Absolute (in ` Crores) | YOY Growth |

|---|---|---|

| Q3FY24 | ||

| Total Assets | 13,98,541 | 14% |

| Net Advances | 9,32,286 | 22% |

| Total Deposits | 10,04,900 | 18% |

| Shareholders' Funds | 1,42,984 | 9% |

| Key Ratios | Absolute (in ` Crores) | |

|---|---|---|

| Q3FY24 / 9MFY24 | Q3FY23 / 9MFY23 | |

| Diluted EPS (Annualised in `) | 77.86 / 76.10 | 74.60 / 65.90 |

| Book Value per share (in `) | 464 | 425 |

| Standalone ROA (Annualised) | 1.75% / 1.77% | 1.92% / 1.73% |

| Standalone ROE (Annualised) | 18.07% / 18.46% | 19.34% / 17.58% |

| Cons ROA (Annualised) | 1.84% / 1.80% | 2.00% / 1.76% |

| Cons ROE (Annualised) | 18.61% / 18.86% | 19.81% / 18.04% |

| Gross NPA Ratio | 1.58% | 2.38% |

| Net NPA Ratio | 0.36% | 0.47% |

| Basel III Tier I CAR ^ | 14.18% | 16.15% |

| Basel III Total CAR ^ | 16.63% | 19.51% |

^ including profit after tax for 9M

18% YOY (a) 18% YOY (b)

18% YOY (a) 18% YOY (b)

CASA

CASA

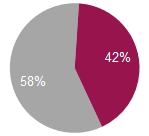

12% YOY (a) | 13% YOY (b)

(a) Period end balances (b) Quarterly average balance

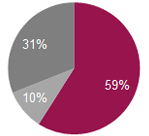

22% YOY (c) 23% YOY (d) Retail

Retail

SME

SME

Corporate

Corporate

27% YOY | 26% YOY | 13% YOY (c) 15% YOY (d)

(c) Overall (d) Overall (gross of IBPC sold)

16% YOY 16% YOY

Healthy operating performance

Strong loan growth delivered across all business segments

Retail term deposits gaining traction, CASA ratio among the best in the industry

Well capitalized with self-sustaining capital structure

Continue to maintain strong position in Payments and Digital Banking

Declining slippages, gross NPA and credit cost

Key domestic subsidiaries7 continue to deliver steady performance

1 QAB – Quarterly Average Balance,

2 Liquidity Coverage Ratio,

3 across 64 global banks, 82 fintechs and 9 neo banks with 2.4 mn+ reviews

4 Monthly active users, engaging in financial and non-financial transactions,

5 (specific+ standard+ additional + COVID)

6 Annualized

7 Figures of subsidiaries are as per Indian GAAP, as used for consolidated financial statements of the Group