Strong CASA and fee performance, accelerating loan growth in focus segments, limited restructuring, improving asset quality, resilient balance sheet

Strong growth in granular CASA deposits continues to aid loan growth

Loan growth driven by focused business segments

Fee up 17% YOY, PAT up 86% YOY

Well capitalized with adequate liquidity buffers

Continue to maintain strong position in Digital

Limited restructuring, dominantly secured, high provision buffers

Key subsidiaries delivered strong performance

1. SBB : Small Business Banking

2. including profit for H1FY22

QAB: Quarterly Average Balance

Coverage Ratio = Aggregate provisions (specific + standard + additional + Covid) / IRAC GNPA

Standard Assets Coverage Ratio (SACR) = Standard asset provisions plus additional provisions plus Covid provision / Standard loans

Snapshot (As on September 30th, 2021) (in ` Crores)

| Profit & Loss | Absolute (in ` Crores) | QOQ | YOY Growth | |||

|---|---|---|---|---|---|---|

| Q2FY22 | Q1FY22 | H1FY22 | Q2FY22 | Q2FY22 | H1FY22 | |

| Net Interest Income | 7,900 | 7,760 | 15,660 | 2% | 8% | 9% |

| Fee Income | 3,231 | 2,668 | 5,899 | 21% | 17% | 34% |

| Operating Expenses | 5,771 | 4,932 | 10,703 | 17% | 36% | 34% |

| Operating Profit2 | 5,928 | 6,186 | 12,114 | (4%) | (11%) | - |

| Net Profit | 3,133 | 2,160 | 5,293 | 45% | 86% | 89% |

2 Prior year numbers are restated to reflect the change in presentation of income from recoveries and provision for depreciation on investments as per guidelines issued by RBI in Aug 21

| Balance Sheet | Absolute (in ` Crores) | YOY Growth | ||

|---|---|---|---|---|

| Q2FY22 | ||||

| Total Assets | 10,50,738 | 17% | ||

| Net Advances | 6,21,719 | 10% | ||

| Total Deposits^ | 7,36,286 | 18% | ||

| Shareholders' Funds | 1,07,083 | 10% | ||

^ period end balances

| Key Ratios | Absolute (in ` Crores) | |

|---|---|---|

| Q2FY22 / H1FY22 | Q2FY21 / H1FY21 | |

| Diluted EPS* (in `) (Q2/H1) | 40.42 / 34.34 | 22.59 / 19.29 |

| Book Value per share (in `) | 349 | 319 |

| ROA* (Q2/H1) | 1.19 / 1.03 | 0.73 / 0.60 |

| ROE* (Q2/H1) | 12.72 / 10.92 | 7.95 / 6.86 |

| Gross NPA Ratio | 3.53% | 4.28%** |

| Net NPA Ratio | 1.08% | 1.03%** |

| Basel III Tier I CAR1 | 17.54% | 16.52% |

| Basel III Total CAR1 | 20.04% | 19.38% |

* Annualised

1 including profit for H1FY22

** as per IRAC norms; for like to like comparison

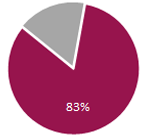

18% YOY

18% YOY

CASA+RTD#

CASA+RTD#

16% YOY (QAB#) | 15% YOY (End Balance)

#QAB - Quarterly Average Balance

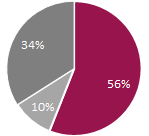

10% YOY Retail

Retail

SME

SME

Corporate

Corporate

16% YOY | 18% YOY | 1% YOY

86% YOY

60% YOY

60% YOY** as per IRAC norms; for like to like comparison

Strong growth in stable and granular CASA deposits

Loan book growth of 10% YOY driven by focused business segments

Net profit at `3,133 crores, up 86% YOY, Fee grew 17% YOY

Retain strong position in Digital Banking and Payments

Well capitalized with adequate liquidity buffers

Limited restructuring, dominantly secured, high provision buffers

Bank’s domestic subsidiaries deliver strong performance, annualized profit closer to ~ `1,025 crore

* Net Interest Margins

1 QAB – Quarterly Average Balance

2 LCR – Liquidity Coverage Ratio

3 Statutory Liquidity ratio

4 Figures of subsidiaries are as per Indian GAAP, as used for consolidated financial statements of the Group

5 compared to Sep-20 figures as per IRAC norms