- Current Account

- Pay

- Collect

- Trade

Services

Solution for Exporters

- Debt & Working Capital

24x7 Loans

For MSMEs with turnover up to ₹30 Cr

- Treasury

- Transact Digitally

Total Amount Payable

3,14,408

3,00,000Principal Amount

14,408Interest Amount

| Year | Opening Balance | Interest paid during the year | Principal repaid during the year | Closing Balance |

| 1 | 300000 | 14408 | 300000 | 0 |

Input loan amount: Start by entering the loan amount you're aiming for.

Set interest rate: Input the competitive interest rate provided by Axis Bank.

Determine loan tenure: Select the duration over which you wish to spread your loan repayments.

Instant EMI reveals: Our calculator swiftly computes your monthly EMI, providing immediate clarity.

Amortisation details: Consult the amortisation schedule for a thorough understanding of your repayment structure, mapping out principal and interest across the loan term.

Start the journey to your dream home today with our Home Loan EMI Calculator. It helps you to explore more options, get a clear picture of the interest rates for ₹30 lakh and ₹50 lakh Home Loans, and plan your financial path with confidence. Axis Bank is committed to offering personalised guidance at every step of your Home Loan journey.

A House Loan EMI calculator is a free online tool that calculates the Equated Monthly Installment (EMI) that you need to pay to repay your loan amount. You can find out your monthly EMI in seconds by merely entering the loan amount, interest rate and loan tenure in their designated boxes.

Key components

Apart from basic calculations, the Axis Bank advanced Housing Loan calculator provides a deeper understanding of your loan and structure. The calculator also provides you with an annual amortisation schedule that allows you to plan your loan repayment scenario better. Your amortisation schedule helps you understand how your interest decreases as your principal decreases.

The housing loan calculator also allows you to experiment with different loan scenarios before deciding on one. By adjusting and readjusting the variables multiple times, you can find the best-suited borrowing structure that aligns with your financial goals and helps you make an informed decision.

Dreaming of your own space? Whether it's a sprawling apartment or a snug bungalow, the journey to your dream home is now simpler. Our Home Loan EMI calculator is your go-to partner for crafting a financial plan that turns dreams into addresses.

This user-friendly Home Loan calculator is designed to give you control over your finances. With just a few clicks, you can set the loan amount and duration that sync with your budget and lifestyle. Adjust the inputs in our Home Loan EMI Calculator to see customized options that help you make well-informed financial decisions. The calculator accurately accounts for current interest rates, guiding you to strategies that minimize the interest paid over the life of your Home Loan.

Take advantage of our calculator to balance your finances and pave a smooth path to the home you've always wanted. It's more than a calculator—it's your financial compass for the exciting journey ahead.

Begin your home-buying journey with a clear financial plan by using our Home Loan EMI calculator online. It's a pivotal tool for:

At Axis Bank, we accompany you as you navigate through the significant milestone of home ownership. Our Home Loan EMI calculator is a cornerstone among the bespoke tools we offer, crafted to optimise your Home Loan experience and maximise your savings on interest payments.

The Axis Bank Home Loan Calculator offers multiple advantages when you are in the process of getting your dream home

Using the Axis Bank's House Loan EMI calculator is straightforward and requires just a few simple steps. Here’s how you can do it:

Start the journey to your dream home today with our Home Loan EMI Calculator. It helps you to explore more options, get a clear picture of the interest rates for ₹30 lakh and ₹50 lakh Home Loans, and plan your financial path with confidence. Axis Bank is committed to offering personalised guidance at every step of your Home Loan journey.

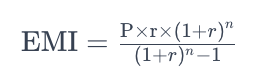

The EMI amount for a Home Loan calculator is calculated using a standard financial formula. Your EMI amount is calculated using your principal amount, interest rate and loan tenure.

Where:

Example: For a ₹20 lakh loan at a 7.5% annual interest rate over 10 years, the EMI would be calculated as:

EMI: 20,00,000 x 0.00625 x (1 + 0.00625)^120 divided by [(1 + 0.00625)^120 - 1]

So, the EMI per month will be ₹23,740 for 10 years or 120 months.

This formula considers compound interest, giving you a precise monthly payment amount. You can calculate the EMI beforehand using this formula or our online Home Loan calculator. It helps you understand how different variables can affect your monthly payments, empowering you to make well-informed financial decisions on the loan amount and tenure that best suit your financial situation.

Axis Bank's Home Loan EMI Calculator is an indispensable online tool for prospective homeowners. This calculator simplifies complex calculations, offering a quick peek into your future financial commitments when considering a Home Loan.

Features:

Benefits:

Axis Bank offers Home Loans for a minimum of ₹3 lakhs, offering a flexible starting point for people to address their home financing needs.

Your Home Loan EMI is due on a fixed date each month, as specified in your loan agreement. Axis Bank offers its customers the flexibility of the auto-debit option, which allows the EMI to be seamlessly deducted from your bank account without any hassle. All you have to do is maintain enough funds in your linked account for the deduction to take place.

The EMI for your Home Loan starts once the entire loan amount has been disbursed. In case of partial disbursement, you will have to pay pre-EMI until the entire loan amount is disbursed.

Pre-EMI interest refers to the interest payable on the loan amount disbursed, applicable until the full loan is disbursed and regular EMIs begin. Unlike standard EMIs that reduce principal, pre-EMI payments cover only the interest on the disbursed amount.

To change your Home Loan EMI date, you will have to submit an official request to Axis Bank via their app or website or by visiting them physically. You can change your EMI date only once every year to maintain discipline. It takes an average of 7-10 working days to process your request.

A Home Loan amortisation schedule provides a detailed overview of your loan repayment process. It breaks down each monthly EMI, showing how much is allocated toward repaying the principal and how much goes toward covering the interest.

Axis Bank does not guarantee accuracy, completeness or correct sequence of any the details provided therein and therefore no reliance should be placed by the user for any purpose whatsoever on the information contained / data generated herein or on its completeness / accuracy. The use of any information set out is entirely at the User's own risk. User should exercise due care and caution (including if necessary, obtaining of advise of tax/ legal/ accounting/ financial/ other professionals) prior to taking of any decision, acting or omitting to act, on the basis of the information contained / data generated herein. Axis Bank does not undertake any liability or responsibility to update any data. No claim (whether in contract, tort (including negligence) or otherwise) shall arise out of or in connection with the services against Axis Bank. Neither Axis Bank nor any of its agents or licensors or group companies shall be liable to user/ any third party, for any direct, indirect, incidental, special or consequential loss or damages (including, without limitation for loss of profit, business opportunity or loss of goodwill) whatsoever, whether in contract, tort, misrepresentation or otherwise arising from the use of these tools/ information contained / data generated herein.

Get to know the eligible amount you qualify to buy your dream home in seconds. Use our Home Loan Eligibility Calculator and start your journey now.

Investing in Fixed Deposits (FDs) offers a reliable and secure means to grow your wealth.

Look through our knowledge section for helpful blogs and articles.

Copyright@ 2025 Axis Bank